Toronto’s condo market in 2026 is one of the most misunderstood opportunities in Canadian real estate.

Prices have corrected from peak 2022 levels. Investor sentiment is cautious. Immigration has slowed temporarily.

And yet, this is exactly where long-term opportunities are created.

If you’re thinking about investing in Toronto real estate, this guide will walk you through:

Why 2026 is a strategic entry point

Where to invest

What to watch for

How financing works (including for Canadians abroad)

Return on investment by the numbers

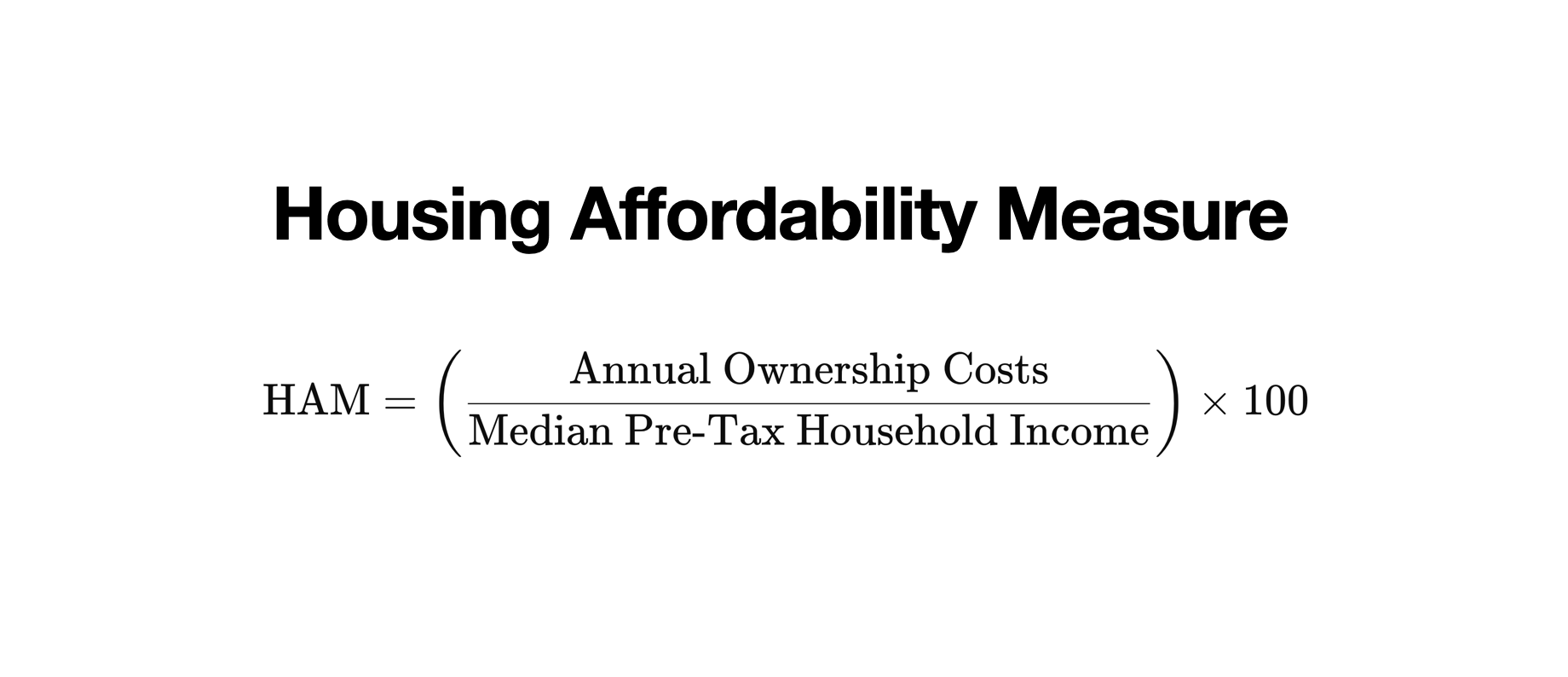

Let’s break it down by the numbers, Real estate vs. S&P 500 Stocks. I’ll walk you through a clear, data-backed view of your return on investment, using market insights and detailed calculation from hundreds of properties I’ve helped investors buy and sell over the years. No hidden gimmicks, just full transparency.

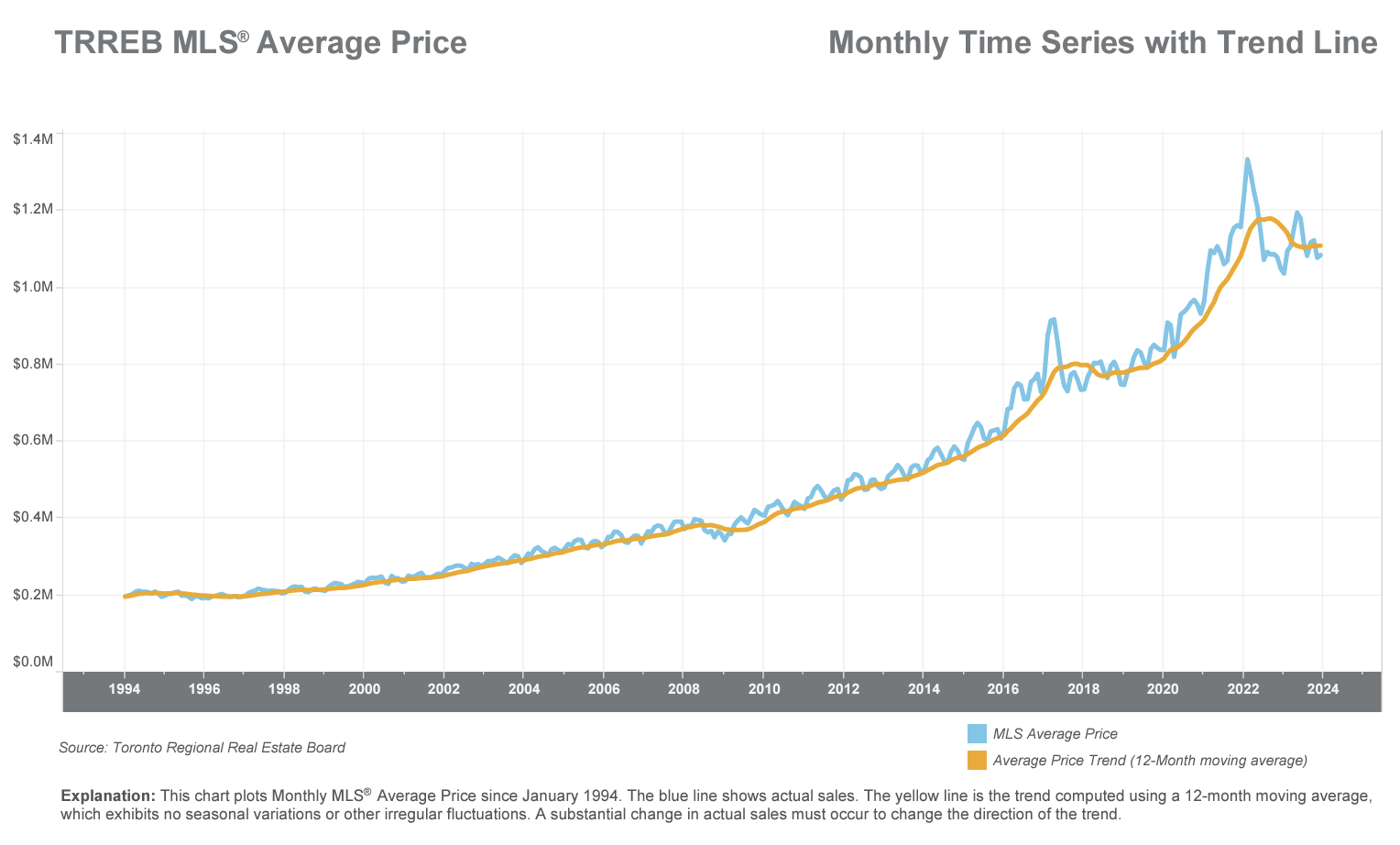

Why 2026 Is a Strategic Entry Point

After years of aggressive growth, Toronto’s condo market has reset.

Prices are down from speculative peaks

Pre-construction pricing has disconnected from resale

Investor activity has slowed

But here’s what matters:

1. Supply Is Drying Up

Housing starts in Toronto have been at multi-year lows since 2024.

This is critical.

Because what gets built today determines supply in 2027–2029.

Fewer starts today = fewer units tomorrow.

2. Immigration Is Slowing But Not Stopping

Canada reduced immigration targets in 2025, which created short-term softness.

But:

Toronto still attracts 35–40% of newcomers

It remains the top economic hub in Canada

Demand may fluctuate but structurally, it’s still strong.

3. Long-Term Imbalance Is Building

When you combine:

Lower construction

Population growth

Urban job concentration

You get a likely supply shortage by 2027–2028 especially in central Toronto. This is where smart investors position early.

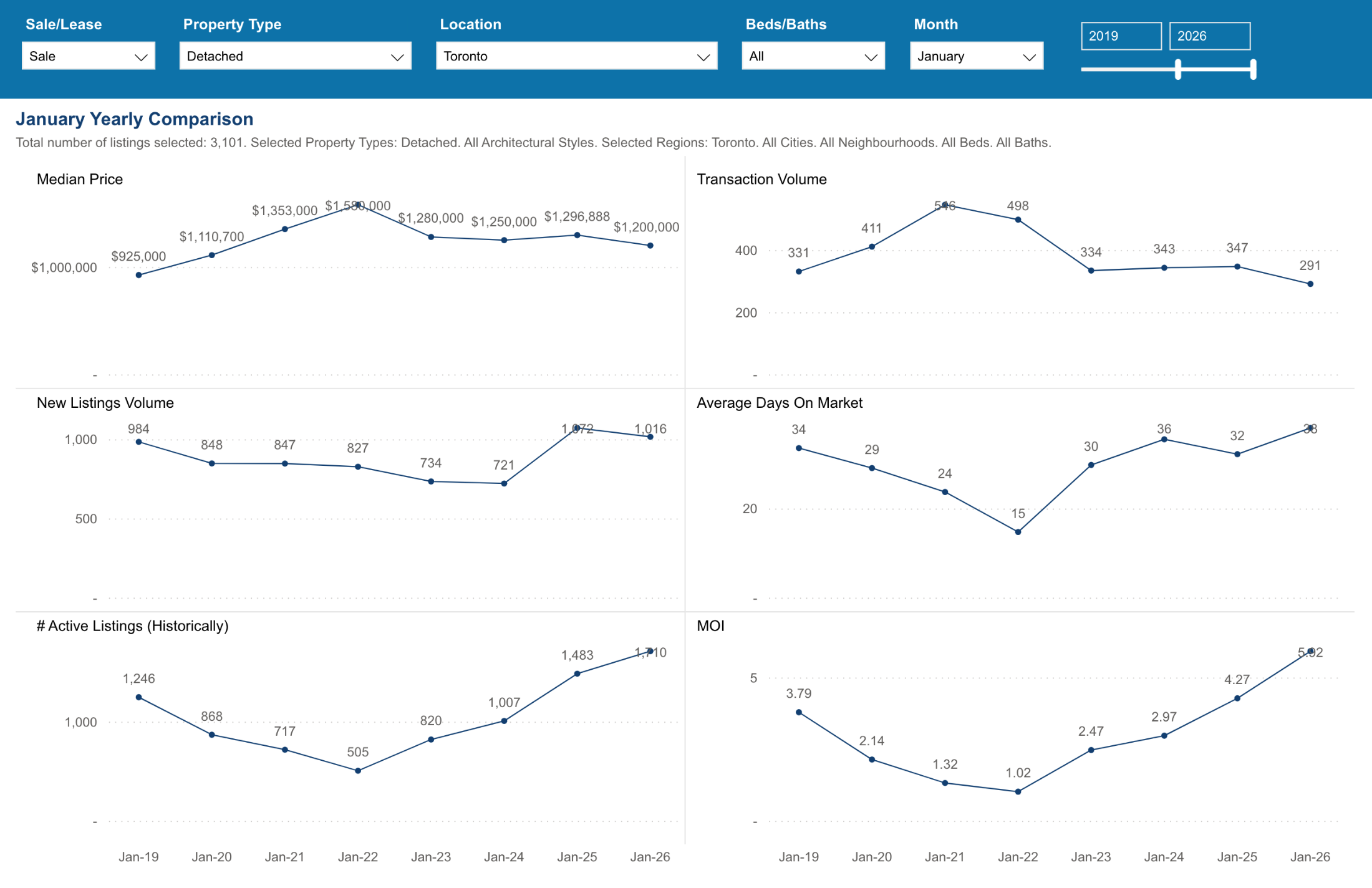

Where to Invest in Toronto

Not all condos are equal. Focus on neighbourhoods with:

Strong transit access

Lifestyle appeal

Long-term demand drivers

High-Conviction Areas:

Yorkville – premium, low supply, global appeal

King West – young professionals, high rental demand

Leslieville / Riverside – lifestyle + growth corridor

Distillery District / Canary District – master-planned + Ontario Line upside

Liberty Village – high rental liquidity

Also look near:

Future Ontario Line stations

Waterfront revitalization zones

Major employment nodes

What Makes a Good Condo Investment

In 2026, investing is no longer about speculation, it’s about fundamentals.

Look for:

Efficient layouts (no wasted space)

Functional 1+1 or 2-bedroom units

Reasonable maintenance fees

Strong building management

Rental-friendly buildings

Avoid:

Overpriced pre-construction

Poor layouts

Buildings with high investor turnover and weak management

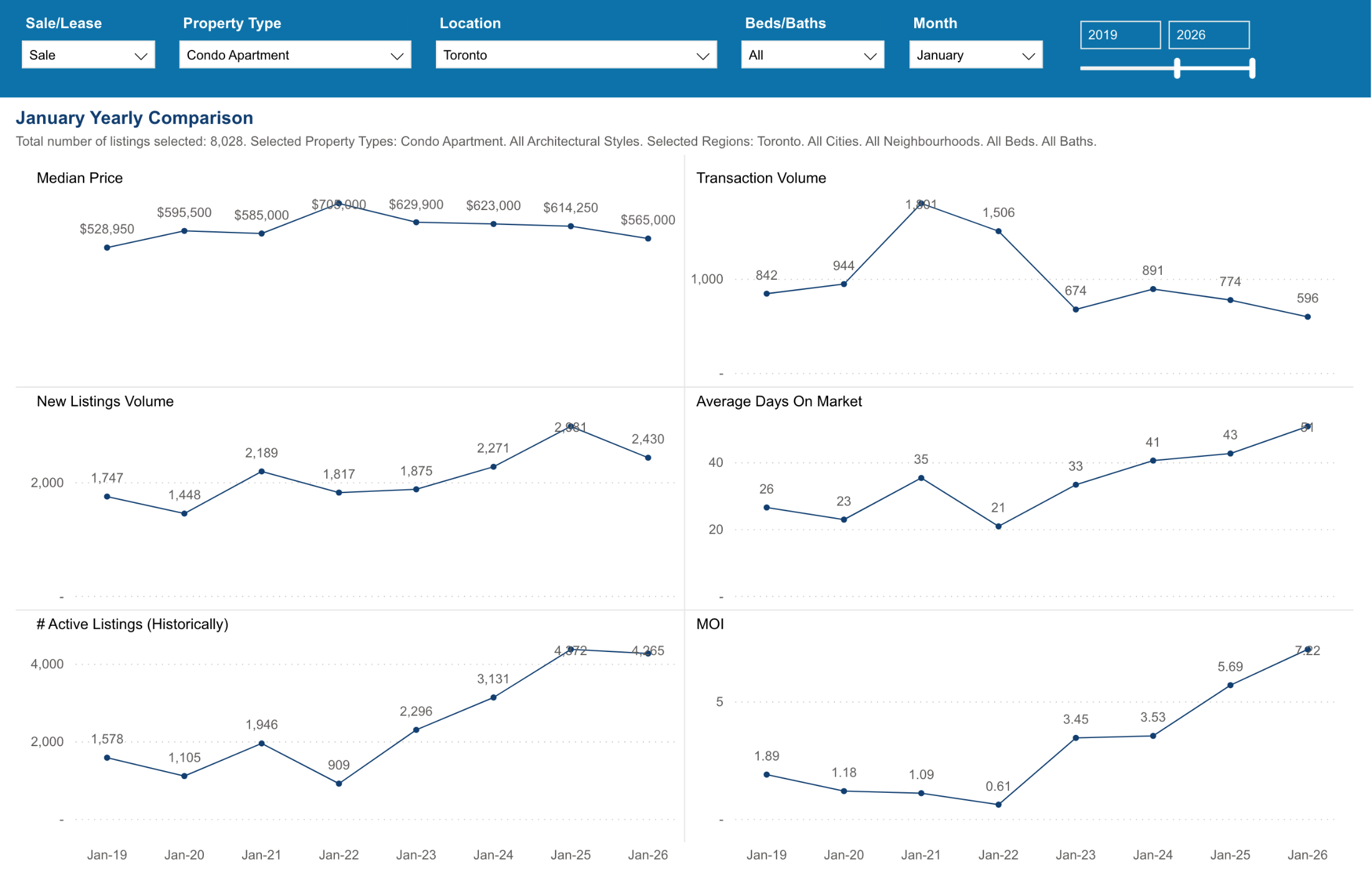

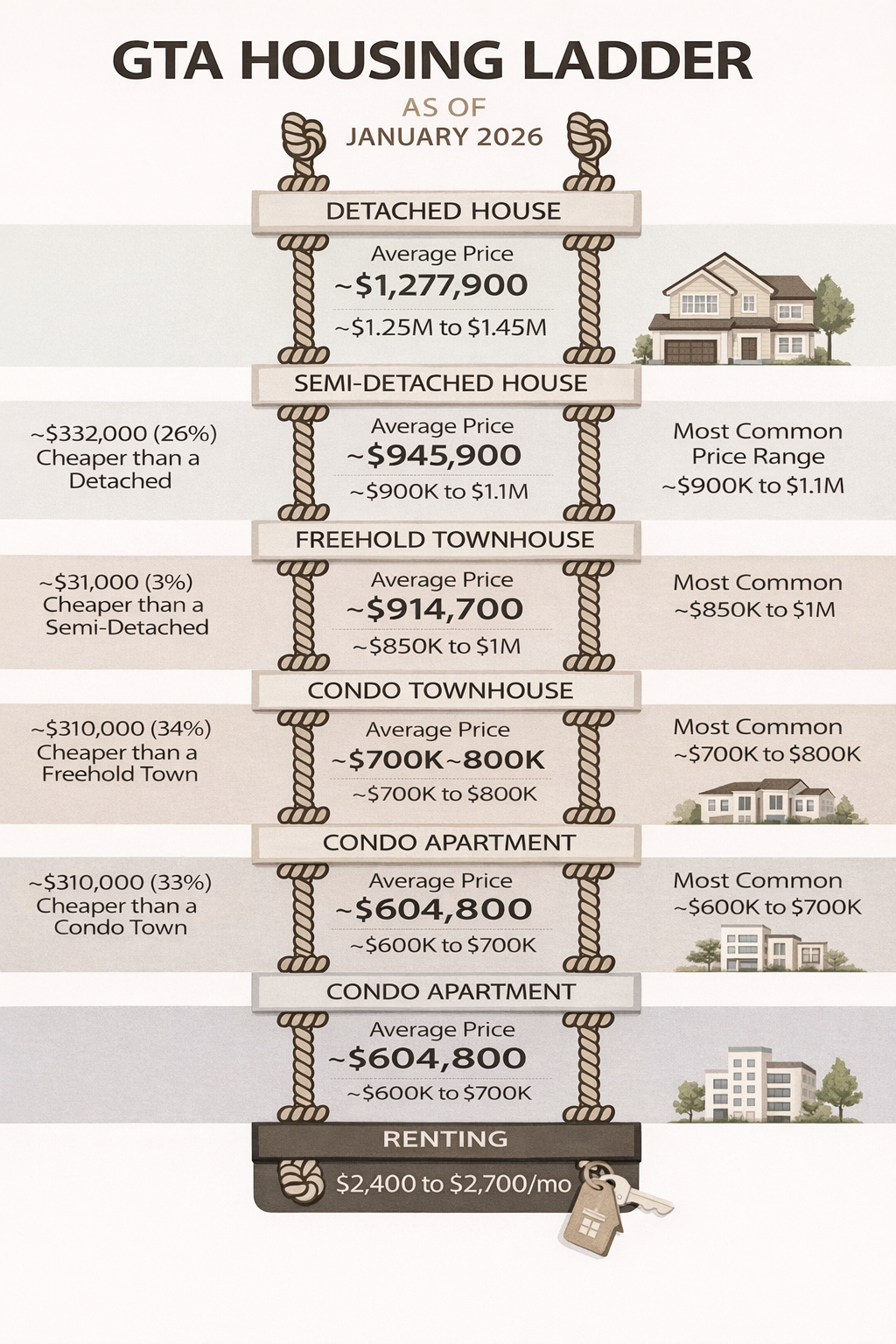

The Numbers: Condo Pricing in 2026

Typical ranges:

1-bedroom: $550K – $650K

2-bedroom: $750K – $900K

Rental income:

1-bedroom: $2,400 – $2,800/month

2-bedroom: $3,200 – $3,800/month

This creates a more balanced environment where:

Cash flow may be tight

But long-term appreciation becomes the play

Step-by-Step: How to Invest in Toronto

1. Confirm Eligibility

To invest in Toronto real estate, you typically need:

Canadian citizenship or permanent residency

Or eligibility under current foreign buyer regulations

2. Build Your Financing Strategy

Understand your down payment capacity

Review mortgage options

Factor in closing costs and holding costs

3. Choose the Right Asset

Focus on:

Location

Layout

Building quality

Not hype.

4. Work With a Data-Driven Realtor

You want someone who:

Understands market cycles

Can analyze price per square foot

Identifies undervalued opportunities

5. Plan Your Exit Strategy

Before you buy, know:

Will you rent it?

Hold long-term?

Sell in 5–10 years?

Clarity upfront = better decisions.

Financing for Canadians Living Abroad (New York, London, Dubai, Kuwait, Saudi Arabia, etc.)

If you’re a Canadian citizen living and working abroad, you fall under non-resident mortgage programs.

Here’s what you need to know:

Down Payment Requirements

Minimum 35% down payment

No exceptions typically offered by major banks

Credit Requirements

Canadian credit history is still required

Lenders typically want:

At least 2 active trade lines

Minimum $3,000 combined limits

2-year history

Additionally:

A foreign credit bureau report (e.g., from Dubai) must be provided

Income Verification

If employed, lenders will require:

3–6 months of bank statements

Pay stubs to match deposits

Statements must be in English (or professionally translated)

Banking Requirements

You must open a Canadian bank account

Mortgage payments must be withdrawn from Canada

Important Limitations

No pre-approvals for non-residents

Lenders only review files once you have an accepted offer

Closing Requirements

You must be physically present in Canada to sign

Virtual signing from abroad is not permitted

Offer Strategy Tip

If buying resale:

Include a financing condition (minimum 5 business days)

This protects you while the lender reviews your file

The Reality of Investing in Toronto

Toronto is not a passive investment market.

It’s:

Competitive

Capital-intensive

Long-term focused

But it’s also:

One of the most resilient real estate markets in North America

A city driven by immigration, jobs, and global demand

Final Thoughts

2026 is not about chasing quick wins.

It’s about:

Entering at more reasonable price levels

Positioning ahead of future supply shortages

Investing with discipline

The investors who win in Toronto are the ones who:

Think long-term

Buy quality assets

Stay patient

Let’s Build Your Investment Plan

Whether you’re buying in 2026 or planning ahead, it’s never too early to start.

If you want help with:

Market analysis

Identifying opportunities

Structuring your purchase

Let’s connect.

Find a time that works for you, and we’ll build a strategy tailored to your goals.