Owning a home in Canada has always been associated with stability, community, and creating a space aligned with your priorities at different life stages. Whether you're buying your first condo in Toronto, upgrading to a townhouse, or planning for a detached family home, real estate anchors your lifestyle.

But what many Canadians overlook is this:

Homeownership in Canada is also one of the most powerful tax-advantaged wealth-building strategies available.

And it’s not accidental.

Talk to Elie

Beyond Stability: Homeownership as Financial Architecture

Yes, owning a home gives you:

Stability in housing costs

A sense of community

Control over your environment

The ability to design a space aligned with your wellness and priorities

But the deeper advantage lies in how the Canadian tax system is designed.

Canada actively encourages homeownership, particularly for Canadians establishing long-term roots in cities like Toronto, because it strengthens the economy, promotes financial resilience, and builds intergenerational wealth. At the center of this design is one powerful concept:

The Principal Residence Exemption (PRE)

The Principal Residence Exemption (PRE) allows Canadians to sell their primary home without paying capital gains tax on the appreciation, provided it qualifies as their principal residence for the years owned.

This means:

If your home increases in value over 5, 10, or 20 years, you pay zero capital gains tax on that growth.

That is extraordinary.

Compare this with:

Stocks

Businesses

Investment properties

Cryptocurrency

All of these are subject to capital gains tax when sold.

Your primary residence is not.

Why the Government Designed It This Way

The Government of Canada supports homeownership because:

It drives economic activity (construction, services, lending, employment)

It builds household balance sheets

It strengthens communities

It creates long-term financial stability

When capital growth is an integral part of your life and your home sits at the center of it, you’re not just buying shelter.

You’re participating in a system intentionally built to reward you.

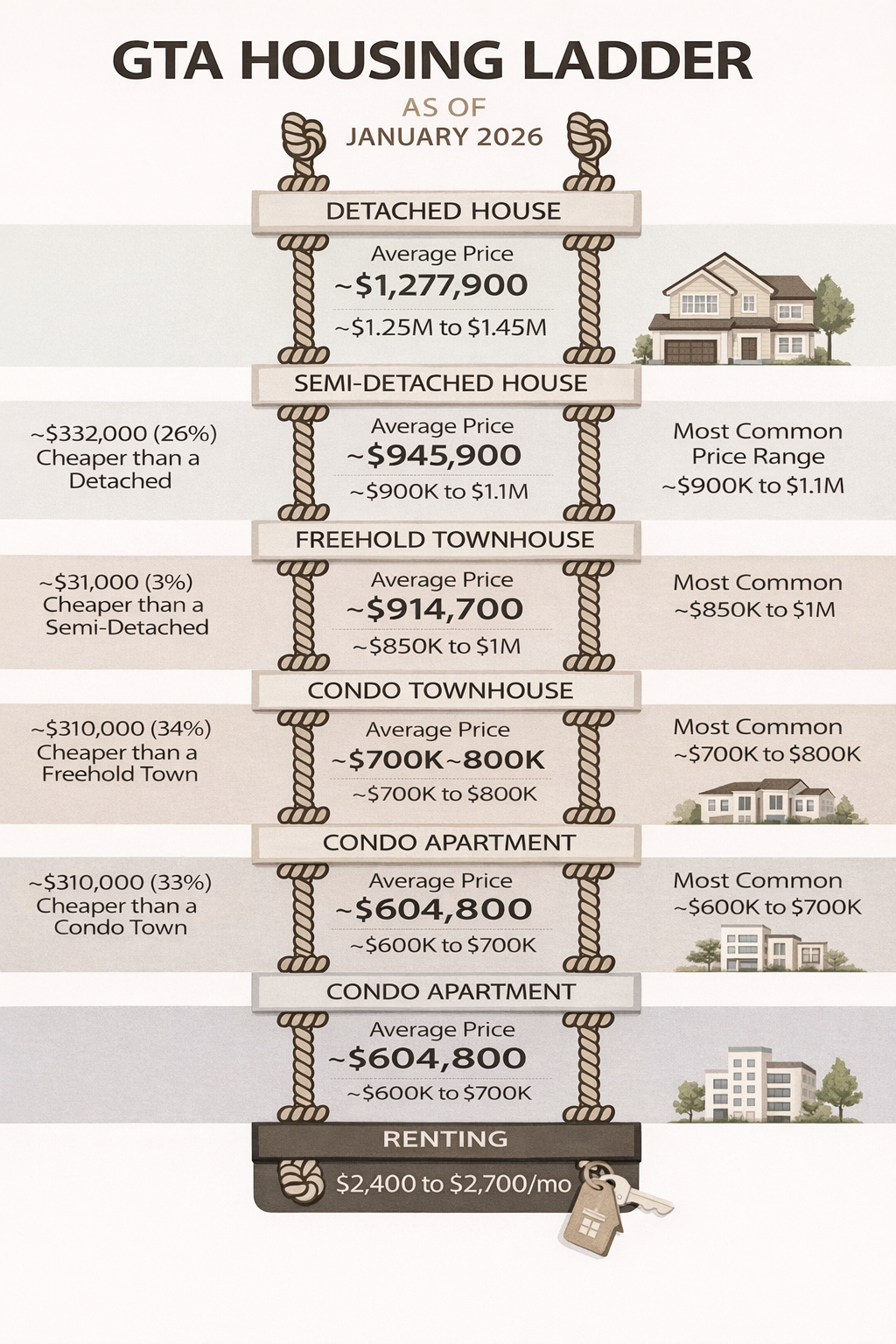

Wherever You Are on the Property Ladder

Whether you’re:

The tax structure remains the same.

Your principal residence is shielded from capital gains tax.

That protection compounds over time.

The Wealth Flywheel: PRE + RRSP Home Buyers’ Plan

Now here’s where it becomes powerful.

When you combine the Principal Residence Exemption with the Home Buyers’ Plan (HBP), you create a financial flywheel.

The Home Buyers’ Plan allows eligible buyers to withdraw up to $60,000 from their RRSP tax-free to purchase a home, provided it’s repaid over time.

This means:

You can use pre-tax savings to acquire an asset

That grows tax-free

And can later be sold tax-free

Side-by-Side Comparison

Adding the Home Buyers’ Plan (HBP)

| Component |

Benefit |

| RRSP Contribution |

Tax deduction upfront |

| HBP Withdrawal |

Up to $60,000 tax-free for purchase |

Example Scenario

Let’s say you purchase a condo in Toronto for $600,000.

Over 10 years, it appreciates to $900,000.

That’s $300,000 in capital growth.

If it’s your principal residence:

You pay $0 in capital gains tax.

If that were stocks:

You would owe tax on 50% of the gain.

That difference alone can be tens of thousands of dollars.

Why This Matters in Toronto

Toronto remains one of Canada’s strongest long-term real estate markets.

When you combine:

Urban growth

Infrastructure expansion (Ontario Line, transit, density)

Population inflow

Government-backed tax sheltering

You create a powerful foundation for wealth building.

Homeownership isn’t just about today’s mortgage. It’s about positioning yourself within a system designed to reward long-term participation.

Important Consideration: Tax Advantages Do Not Guarantee Appreciation

While the Principal Residence Exemption provides one of the most powerful tax shelters available to Canadians, it’s critical to understand the nuances.

Tax protection does not guarantee asset performance.

Not every residential property purchased as a primary residence will appreciate at the same rate and some may underperform relative to broader market averages.

Real estate is not homogeneous.

Long-term equity growth is influenced by measurable fundamentals, including:

Micro-location dynamics

Transit and infrastructure development

Supply pipelines and future inventory risk

Layout efficiency and functional design

Building quality and reserve fund health

Demographic migration patterns

Economic drivers in the surrounding area

Two properties in the same postal code can produce materially different long-term outcomes.

The Principal Residence Exemption shields capital gains from tax, but it does not create them.

Capital appreciation is driven by asset selection. This is where strategic guidance becomes essential.

A disciplined, data-informed acquisition process evaluates not just current market pricing, but long-term value drivers. Over the past decade, I have focused on helping a select group of clients make purchase decisions rooted in fundamentals, not momentum or emotion.

The objective is not simply to “own property.” It is to:

When structured properly, your home serves both your personal priorities and your long-term financial architecture. This is where I come in to advise you on the ideal property fit.

Talk to Elie

Final Thoughts

Owning a home in Canada goes far beyond stability and lifestyle alignment.

It is:

A tax-efficient wealth strategy

A government-supported growth vehicle

A foundation for long-term financial resilience

When structured properly, your home becomes the center of both your life and your capital growth.

If you’d like to understand:

Where you sit on the property ladder

What type of property aligns with your life stage

How to structure your purchase strategically

Or how to combine PRE + RRSP Home Buyers’ Plan effectively

Talk to Elie

Let’s design a plan aligned with your goals, financially and personally.